The commercial real estate industry will fundamentally shift again due to the banking industry in 2020. The Humpty Dumpty that Tim Geitner and Hank Paulson put back together in 2009 is about to re-shift into an entirely new landscape broken up into three sections, retail banking, commercial banking and investment banking.

Banks own multiple different asset classes for a multitude of reasons, but this article will focus on branch consolidation.

Here are the primary reasons why I believe the consolidation is transpiring with such intense rapidity:

Mobile Banking Replacing Bricks & Mortar

Almost every task, except for those requiring hard paper, can be done from a smartphone or tablet.

Overexpansion Before the 2008 Crash

Banks were in a frenzy committing to expensive long-term ground leases. Those terms are starting to expire and will continue until around 2025-2030.

Mergers & Acquisitions

The Truist Merger is on the horizon, and I am confident this monumental consolidation triggers additional M&A’s and business opportunities as the massive, complicated and institutional deal comes to fruition. From what I have read online and heard from friends in Atlanta, SunTrust (I am a client) is taking care of everyone (in terms of compensation) in the merger and living up to their solid and timeless reputation that goes back 108 years to pre-Depression Atlanta, Coca-Cola in its infancy, and Georgia Peach baseball.

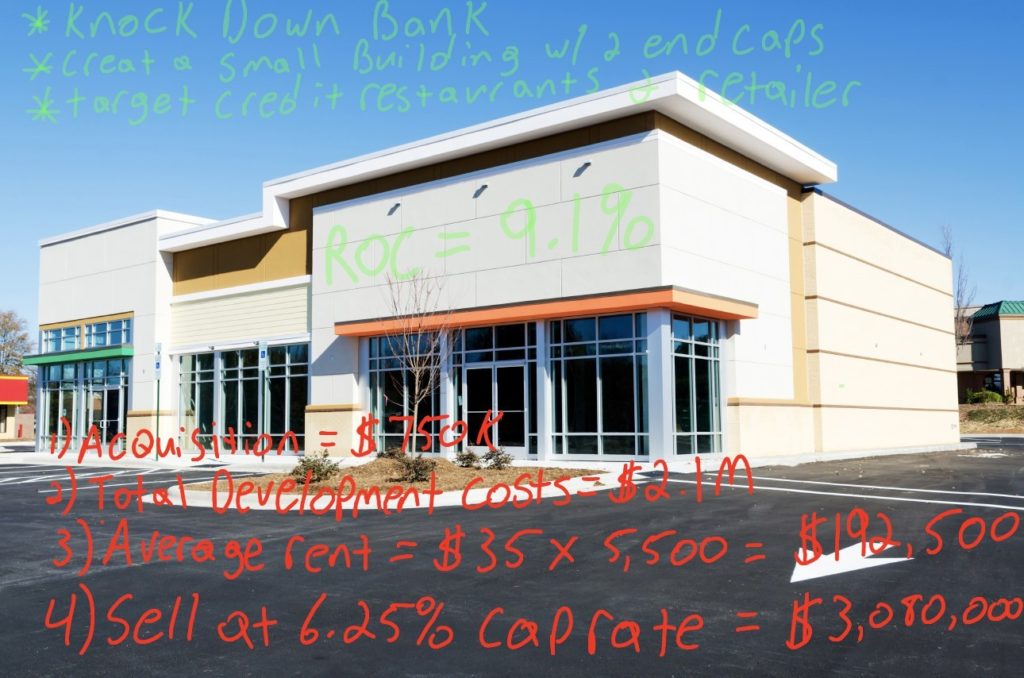

As the consolidation unfolds, opportunities for leasing and disposition will present themselves. Here are some tips on how to lease and sell bank branches:

1) Initial Due Diligence: Bank sites sit on some of the most visible pad sites in commercial real estate. During the expansive early to mid-2000s, banks paid a premium for Tier A real estate and built branches at prominent corners. In many cases, obsolete buildings now need to be redeveloped. Do your homework—especially when it comes to zoning, parking and municipal requirements.

3) Explore Alternative Uses: This is a part of due diligence as well. Most municipalities categorize bank buildings as some variation of the financial institution designation. Look what the process and replacement cost would be to redevelop to a higher and better use.

4) Impact Fee Credits: Banks, which typically have drive-thrus, usually pay over retail price for municipal fees because of their impact on the area’s concurrency. These credits are generally transferable and can help the bottom lines as a paid deal cost.

5) Drive-Thru Uses: part of due diligence as well, but these can be utilized, enclosed to add leasable area, or converted to patios for restaurants.

7) Deposit Research: Go figure out what the banking deposits are. Dig a little, every deposit is public record.

8) Land Lease vs. BTS vs. Disposition: Take a three-pronged approach to each—least ideal to most profitable (from an owner/developer perspective).

Disposition

A developer usually carves out a portion of a property for a few reasons. A developer is undertaking a large project with multiple different asset classes, also called a mixed-use project. A retail developer knows that 300 apartment units would help his grocery-anchored shopping center, but multi-family development isn’t their specialty. In most cases, they will flip the parcel to a designated specialist. They need additional liquid capital or the cash from the flip, and this quick cash infusion can help with development costs, marketing costs or pay down debt.

Build-To-Suit

The developer typically builds a vanilla shell or a modified shell to the tenant’s specs. This structure also implicitly has more substantial development and management fees. The inherent risk is your vacancy factor, how re-leasable space is and that you could get stuck with a tenant-specific building. Mimi’s Café is an excellent example because, when they closed all locations, their build-out was so unique that the national chains avoided their structure due to intrinsic obsolescence.

Ground Lease

These are ideal because they pose a nominal risk. The land and building revert to the landlord when the tenant vacates. The upfront cost is minimal, and the profit usually significant if executed adequately. The upfront capital is provided by the tenant, further hedging exposure. McDonald’s is the gold standard of creditworthiness and the picture above is of a lease that was signed in 2013 in Lake Mary, FL. I represented the landlord and had the pleasure of working with my friend James Mitchell at CBRE on this deal, which traded at sub-5 cap rate, which was monumental at the time.

Technology is changing the world and bank branches were the backbone and physical representation of entrepreneurialism for decades. Time and digital interaction expedited their physical obsolescence, but tectonic consolidation is fundamentally shifting the bank sector of commercial real estate and will create opportunities for the banks to reorganize and redefine their brand. It will also allow for REITs, brokers, building owners, and developers to reshape, regenerate and invigorate our communal landscape.